Continuing on our journey of navigating the maze of insurance – let’s continue with the next line of coverage.

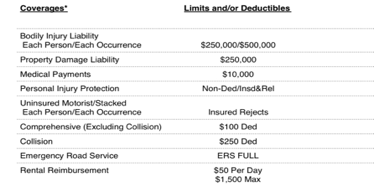

Medical Payments, or Med Pay, pays for YOUR medical bills, due to an accident. This can cover the costs such as: an ambulance, hospital stays for you, and those in your vehicle.

Personal Injury Protection, or PIP, is coverage that pays for medical expenses. PIP is extremely important in No-Fault states. A No-Fault state is a state where it doesn’t matter who caused the accident. Each driver’s policy will pay for their own medical expenses, however, the at-fault driver’s policy will pay for property damage.

Example

Kim, Tim, and Jacob all live in Michigan. Kim’s policy would still owe for Tim and the City’s damaged property, but both Tim and Kim’s individual policy would need to be filed against for medical expenses.

There are 12 states in the United States that are “No-Fault” states. They are:

- Hawaii

- Utah

- North Dakota

- Michigan

- Kansas

- Minnesota

- Kentucky

- Florida

- New Jersey

- New York

- Pennsylvania

- Massachusetts

Next up is Uninsured and Underinsured Motorist Coverage. This is very important. Some states mandate that your policy carry this coverage, others make it an option. These twin coverages can be the unsung heroes of your policy, as these coverages can trigger when a person either does NOT have ANY auto insurance (uninsured) or doesn’t have enough coverage (underinsured) to cover your medical bills.

Too often, I have witnessed customers get what’s called the State Minimums. This is the least amount of insurance needed to satisfy state requirements to drive. If you get into moderate accident, or hit more than one vehicle, you can easily exceed the state minimum coverage limit requirements.

For most states, that can be a combination of $25,000/$50,000 for Bodily Injury and $10,000 for Property Damage.

It’s often written like this $25/$50/$10 or $25,000/$50,000/$10,000.

The consumer will either not elect to carry Uninsured/Underinsured Motorist coverage, or it will match the limits of $25,000/$50,000. (If you’re confused on what BI/PD, I recommend you go back to the Article Entitled Auto Insurance 101.)

According to a study completed by MoneyGeek.com (Wack, 2022), 1 out of every 8 drivers went without insurance in the US. That total number was 28 Million Drivers. All it takes is one bad day, one distraction, one text message, one eyelash being attached or one egg McMuffin being eaten for something to occur, and that will cause a not so good day!

I’m off my soapbox now….I promise…for now LOL…Well..the next two I might be on a different Soap Box.

The next two coverages are often the most “mis-informed”, they are Comprehensive, or Comp, and Collision coverage. Many people will refer to these two as having “Full Coverage”.

Ladies & Gentlemen…..PLEASE No More Saying FULL COVERAGE.

I get it, it’s easier to say full coverage…except it sets up the expectation that you have coverage for everything….and in reality, you may not.

Comprehensive, or Comp coverage are for things that’s known as “Acts of God”. These can include:

- Lightning

- Fire

- Hailstorm

- Hurricane and Windstorms

- Floods

- Theft of your vehicle

- An animal hitting your vehicle

These are examples, and not the full exhaustive list. A great way to look at it, Comp typically covers things that are out of your control. Please Note I stated typically lol.

Collision coverage, if elected, pays for repairs to YOUR vehicle when an at fault accident has occurred. In our earlier example of Kim hitting Tim’s vehicle, if Kim had Collision coverage, this is what would trigger to make repairs to her vehicle.

Collision may also be triggered even when it may appear like it should be a Comprehensive loss. The best one comes from experience being from the Midwest. We have very courageous deer that will race you, if they spot you. If you’re driving along, and you swerve to miss the deer, and hit the rail guard, because you collided with the guard, and not the deer, this would be a collision loss. If the deer had collided with your vehicle, then it would’ve likely been a Comprehensive loss.

Please Note That Both Comprehensive and Collision, if elected, REQUIRES a deductible. A deductible is your portion that you must pay towards a loss.

The last two coverages discussed are optional, and quite simple. They are Emergency Road Service, or ERS, and Rental Reimbursement.

Emergency Road Service (ERS) can provide services such as: tows, lockout service if you lock your keys in your car, bringing flat tire(s) to your vehicle, if you hit a flat. You will have to purchase the tire. It can also have someone bring you gas, if you run out. You will have to pay for the gas. I recommend having ERS because you never know when you might need it. I also recommend checking with your insurance provider because some offer more services, as a part of their customer experience, and may have stipulations regarding the service, such as a limit on the miles the tow service will provide.

Rental Reimbursement provides a limited amount, that you select, to go towards the rental of a vehicle, while your vehicle is being repaired – DUE TO AN ACCIDENT! I know someone is going to say, “Mike why are you yelling?” I’m not, but I cannot stress the importance of it being due to an accident. As a Sales Agent and Claims Rep, I can’t count how many times I got that question, if a person could rent a vehicle and use their Rental Reimbursement for their weekend vacation vehicle.

…..

Well that wraps up the basics of the auto policy. In later articles, we will discuss the basics of the claims process. Hopefully you have gotten something from this.

Please feel free to comment and give feedback. I can always tweak the articles for more information.

~ Til Next Time!

Wack, M. (2022, November 27). Uninsured motorist statistics 2021. MoneyGeek.com. Retrieved November 27, 2022, from https://www.moneygeek.com/insurance/auto/resources/uninsured-motorist-facts/

Leave a comment